Global| Sep 12 2008

Global| Sep 12 2008BOF Survey Rises Encouraging the Bank to Hold the Line on its Outlook for Growth

Summary

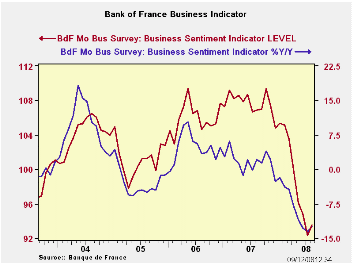

The BOF indicator has been weak and it has been weakening. But in August the indicator put on the brakes, and actually rebounded. While every other EMU country is cutting, chopping or shaving its forecast the BoF has held firm on its [...]

The BOF indicator has been weak and it has been weakening. But in August the indicator put on the brakes, and actually rebounded. While every other EMU country is cutting, chopping or shaving its forecast the BoF has held firm on its outlook armed with this tiny rebound in the context of a steep downtrend in the index.

The BoF projects Q3 growth at 0.1%. The survey points to some slight increase in activity but trends have been diminishing. All readings in the industry survey are below their historic averages. The overall industry index resides in the 13th percentile of its range of values since 1987. Production outlook responses are in the bottom 25 percentile of their ranges. All industries’ production outlooks are weak except for capital goods which amazingly continues to reside in the 88th percentile of its historic range. Consumer goods, in contrast, are in the bottom 14 percentile of their range agriculture and food industries are in the bottom 8 percentile of their ranges.

Order books are weak. Both raw readings slipped this month. For total orders the series resides in about the bottom third of its range. But foreign orders are much weaker and are now in the bottom 5 percentile of their historic range. New orders are also weak month to month.

It is the production outlook and production in the current month readings that have improved in this August survey. This is a current activity series and another based on plans. But if actual orders are so much weaker and if order books are emaciated, why are plans for output so strong? The BoF survey still raises a lot of questions about France’s optimism.

| Bank of France Monthly INDUSTRY Survey | ||||||

|---|---|---|---|---|---|---|

| 12 MO | Since Jan-87 | Ranking | ||||

| Aug-08 | Jul-08 | Jun-08 | AVERAGE | Average | Percentile | |

| Production-latest mo | ||||||

| Total Industry | 4.69 | 2.09 | 0.45 | 3 | 7 | 30.6% |

| Semi-Finished | 4.84 | -4.1 | -0.76 | 2 | 5 | 44.1% |

| Capital | 1.1 | 5.58 | 9.98 | 6 | 7 | 21.2% |

| Auto | 7.76 | 6.32 | -22.28 | -3 | 8 | 53.1% |

| Consumer | 8.42 | 4.48 | 10.68 | 6 | 8 | 50.2% |

| Agric&Food | 5.42 | 1.41 | -0.74 | 4 | 10 | 22.9% |

| Production Outlook | ||||||

| Total Industry | 2.75 | -5.71 | 1.82 | 5 | 7 | 15.5% |

| Semi-Finished | 0.23 | -4.78 | -2.79 | 4 | 6 | 18.4% |

| Capital | 14.98 | 0.54 | 7.8 | 9 | 7 | 88.2% |

| Auto | 3.75 | -13.05 | 10.62 | 14 | 14 | 25.7% |

| Consumer | 10.46 | -3.55 | 8.72 | 9 | 16 | 14.3% |

| Agric&Food | 8.83 | 6.95 | 7.96 | 11 | 16 | 7.8% |

| Demand | ||||||

| Overall order books | -1.63 | 2.6 | 5.36 | 17 | 4 | 36.7% |

| Foreign Orders | -6.91 | -4 | -5.55 | 4 | 8 | 4.9% |

| New Orders | ||||||

| Total Industry | -3.24 | 0.26 | -3.39 | 5 | 8 | 8.2% |

| Semi-Finished | -1.19 | -3.42 | -2.03 | 3 | 7 | 19.6% |

| Capital | 1.86 | 12.92 | -6.11 | 7 | 9 | 24.1% |

| Auto | ||||||

| Consumer | 10.37 | 10.5 | 9.69 | 11 | 11 | 44.1% |

| Agric&Food | -12.21 | 2.72 | -5.94 | 2 | 10 | 0.8% |

| Stocks: Finished Gds | ||||||

| Total Industry | -1.59 | 0.09 | 0.54 | -2 | -2 | 55.9% |

| Semi-Finished | -2.72 | -0.14 | 3.49 | -2 | -2 | 37.1% |

| Capital | 3.8 | 0.94 | 2.08 | -1 | -3 | 95.5% |

| Auto | -18.44 | 6.36 | -11.74 | -5 | -3 | 13.5% |

| Consumer | -3.48 | -0.17 | -0.3 | -1 | 0 | 18.0% |

| Agric&Food | 1.57 | -1.82 | 3.11 | 1 | 0 | 59.6% |

| Capacity Utilization | 80.72 | 81.17 | 81.51 | 83 | 83 | 9.8% |

| Hiring | ||||||

| Latest Mo | -2.82 | -3.37 | -2.47 | -1 | -1 | 44.9% |

| Outlook | -4.52 | -5.48 | -3.62 | -2 | -3 | 73.5% |

| Industry Sentiment Index | 93.55 | 92.35 | 94.86 | 102 | 104 | 13.9% |

| Ranges, percentiles since January of 1988. | ||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief