Swiss HICP inflation in July was zero month-to-month. In June, it was zero month-to-month. In May, it was 0.1% month-to-month. Year-over-year HICP inflation is 0.7%, compared to a year ago when it was 0.1% over 12 months.

The same metrics viewed through the domestic measure of Swiss inflation are even lower. In July, domestic prices rose 0.1%; in June, they fell by 0.1%; and in May, they were unchanged. The 12-month inflation rate for the Swiss CPI in July was 0.4%; a year ago the 12-month change was 0.2%. Pinch me! Am I dreaming?

And yes, Switzerland is on the same planet as the United States, Europe, and the United Kingdom.

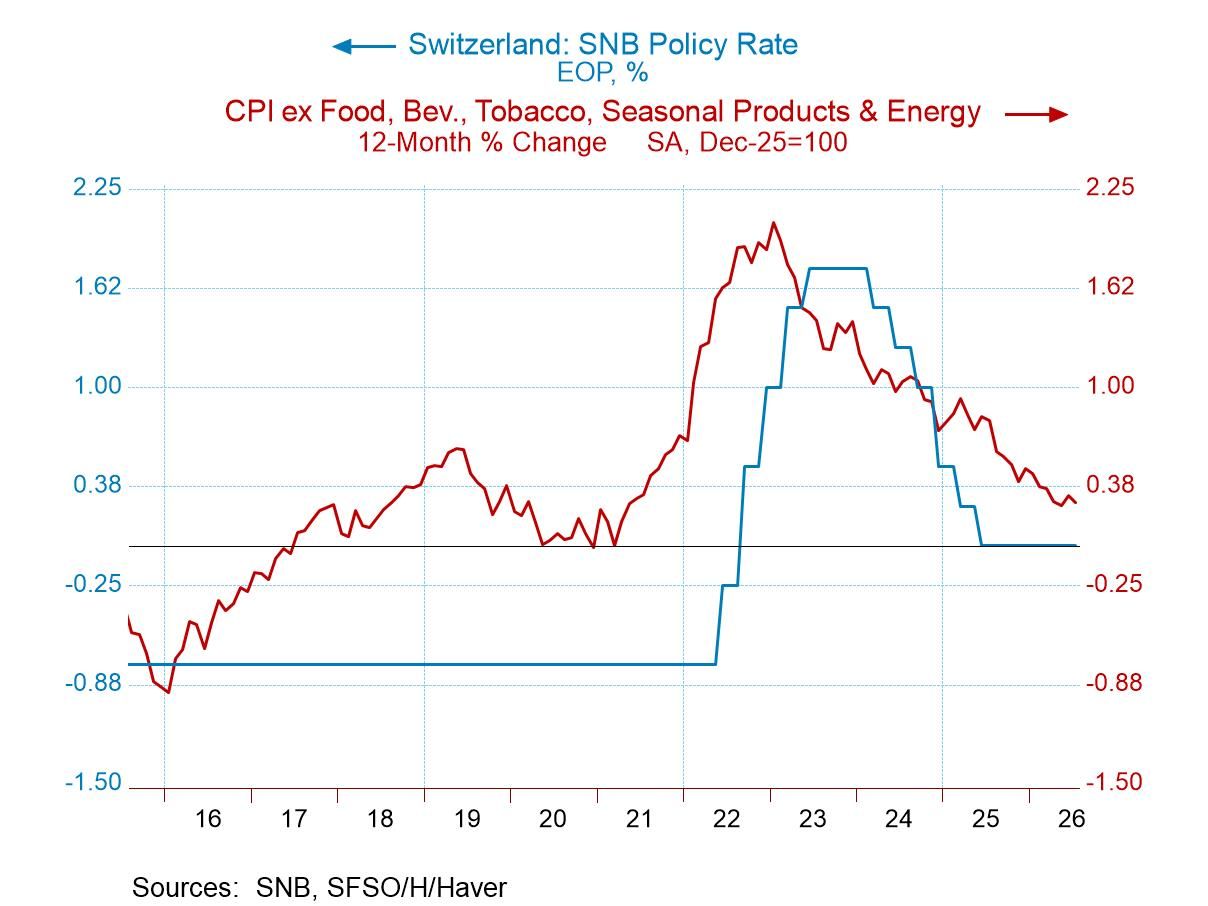

Swiss inflation going back to 2020 has a peak year-over-year rate in its core of 2% based on monthly data. The headline 12-month rate at its peak was 3.4%. Excluding administered prices, the peak inflation rate in Switzerland was 2.7%. One of the main things that Switzerland has going forward is that the Swiss National Bank (SNB) has incredible credibility. It waited as long as the Fed did to raise interest rates, but it raised rates quickly up to the level of the core inflation rate. Once inflation began to fall, the SNB continued to raise rates until it became clear that the policy rate had begun to hover above the inflation rate. At that point, the bank flattened out its rate profile, then turned into a rate-cutting mode.

Once again after the inflation rate had been arrested and fell below 1%, the SNB continued to cut rates until inflation was at zero and so were rates.

The U.S. has not had the same experience with inflation. U.S. inflation has lingered and the Federal Reserve has continued to hold its policy rate above the 12-month trailing inflation rate.

Swiss performance is unique, suggesting that monetary policy right now is not needed to control inflation, at least not in Switzerland. But this undoubtedly has a lot to do with expectations about the behavior of the SNB and the dynamics of the Swiss economy and capital markets.

Swiss inflation began to track the 1% mark in early 2024. The core rate fell into line at the same time, with very little lag. This also is very unlike the U.S. experience.

Global

Global