Global| Aug 22 2024

Global| Aug 22 2024PMIs Firm Globally, Germany Holds Back Europe

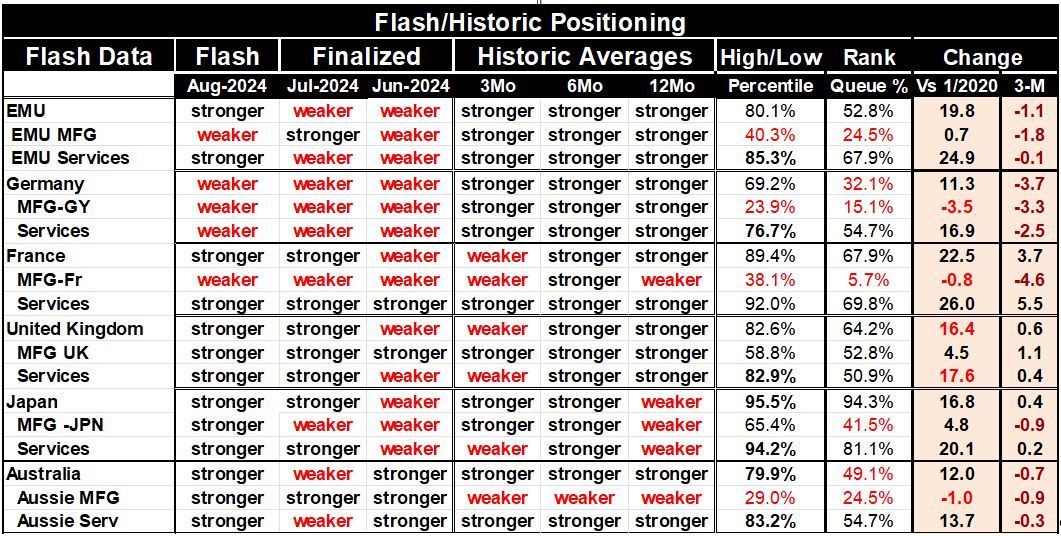

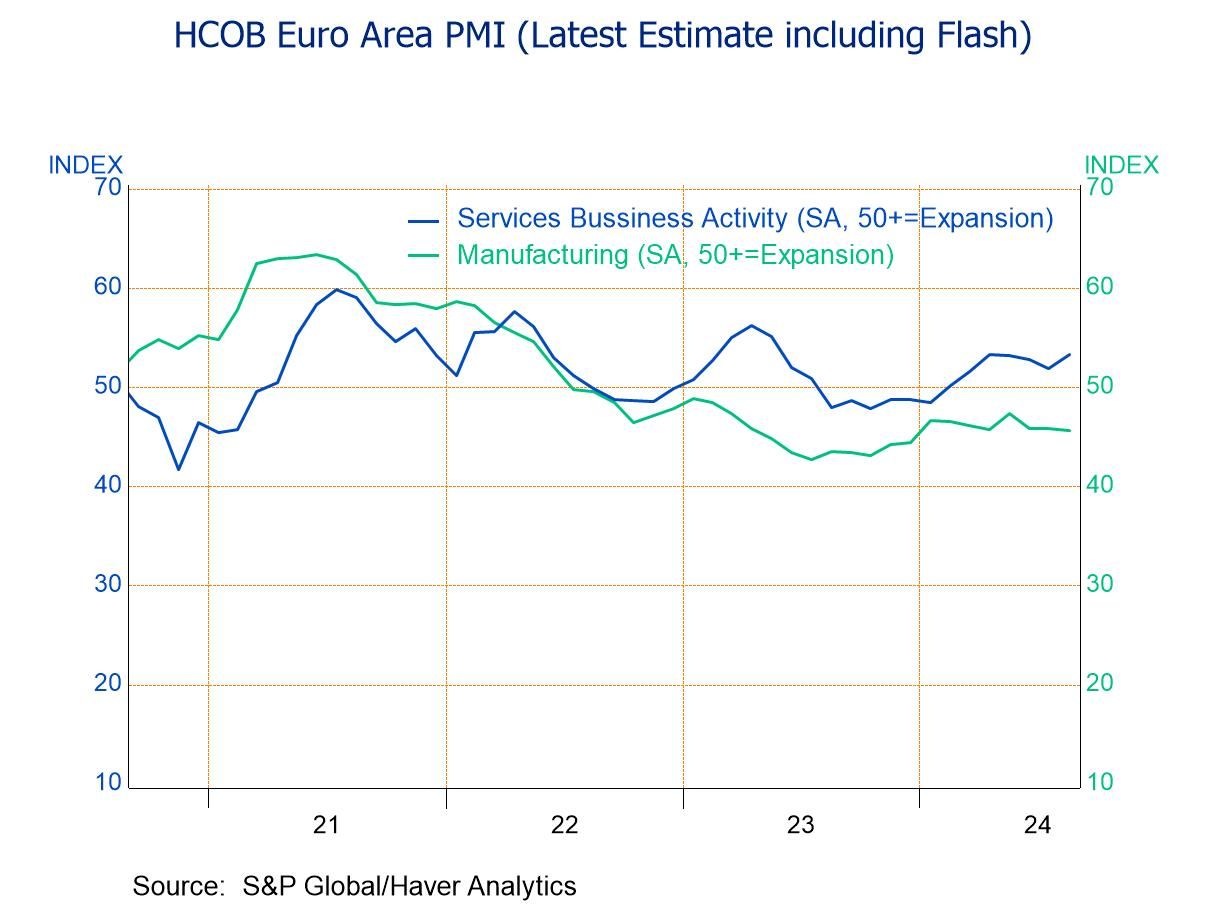

The flash PMI data from S&P for August show a great deal of strengthening by most reporting developed countries. Europe posted a mixed profile in the August report with Germany weakening and it's composite reading as well as in each of its contributing sectors of manufacturing and services. The German situation sees weakening and all three of these measures for each of the last three months. France has weakened in manufacturing in August as well as the previous two months. As the two largest economies in the European Monetary Union, the profile for EMU this month is also held back. The headline for the EMU composite nonetheless posted a gain month-to-month in August and the services sector also posted a gain. Apart from the weak several months of data, the Monetary Union shows that average conditions have been strengthening over 12-months compared to a year ago, and over six-months compared to 12-months, as well as three-months compared to 6-months. And despite the recent weak German data, Germany is also stronger on most metrics sequentially, remembering that in this treatment of data we calculate the historic trend only on completed data, so the performance of the averages begins with data from July backward does not include measures from August.

United Kingdom shows strengthening in its composite services and the manufacturing in August as well as in all three sectors in July, putting a better foot forward after a period of difficulty. The report for the UK this month is encouraging.

Japan also shows strengthening in the composite and manufacturing and its services in August the composite and services improved in July and Japan but manufacturing had been weakening this month’s manufacturing result is a turnaround for the sector in Japan; up to this point, economic data and especially manufacturing data in Japan have not been looking very robust.

Australia shows improvements and the composite manufacturing and in services in August, after seeing only strengthening in manufacturing in July but having seen strengthening in all sectors in June. Australia's averages show the composite stronger over 12-months, 6-months and 3-months dragged higher by a strengthening service sector even as manufacturing was weaker over each of those horizons.

Globally, the services sector has been consistently improved over 12-months, 6-months, and 3-months in most reporting units; Japan has been the most significant exception to that observation.

In terms of broader perspective, the queue standings that rank this month's observations against data going back to 2020 shows that most sectors for most countries have improved their PMI standings to the point that they are above their medians on this timeline. Germany and Australia are the biggest exceptions with below median readings (which means below 50% queue standings) for the composite as well as for the manufacturing sectors. However, Germany is in worse shape with its composite standing in its lower 32nd percentile and with manufacturing at its lower 15th percentile, an extremely weak reading for a country that is dependent on its manufacturing sector and on export-oriented growth. In part because of German weakness, the European Monetary Union manufacturing standing is only in its 24th percentile, however, France also has a very weak manufacturing sector that stands only in its 5th percentile.

Japan this month showed some strong percentile standing with its composite in its 94th percentile and with services and their 81st percentile.

Over the last 3-months on a net basis the European Monetary Union composite has declined, the German composite has declined, and the Australian composite has declined. Composite readings have increased in France, United Kingdom, and Japan on this timeline but by only small amounts for those three countries - except for France.

Manufacturing has weakened over 3-months in all the countries in the table except for the United Kingdom it shows a net gain of about 1.1 diffusion points over the last 3-months.

The service sector weakened modestly in the Monetary Union over the last three months; it fell relatively sharply in Germany over 3-months dropping 2.5 points, while in France the services sector gained 5.5 points, helping to offset some of the weakness in Germany within the Monetary Union. Services improved over 3-months by a small amount in the UK and in Japan; Australia saw a setback. Only Australia, Germany, and the Monetary Union experience declines over 3-months for all three sectors, the composite, manufacturing, and services.

On balance, this an inconsistent set of responses from the S&P report this month, as there is some evidence of firming across countries but Germany, an important and large economy, continues to struggle to get back on the path for growth. Meanwhile, the war between Russian and Ukraine is as hot as ever and become more dangerous as Ukraine has made forays across the Russian border. Conditions now are very much touch and go in the Middle East, with US sending more warships to the area, worried about some sort of reprisal by Iran against Israel. The global shared political situation is about as dangerous as it has been many years. The economic situation is still on the mend with a good deal of weakness is still scattered about and not enough momentum to be sure that an important corner has been turned. A great deal of progress on inflation has been made globally but recently inflation process has stalled across Europe and in the US leaving it unclear as to what central banks do next even though most of them have either given us guidance that they're headed for an easing path or have already stepped onto that path. Those central banks that have already begun to make their way in an easing environment have slowed and brought their easing to a halt as they appraise the recent and changing inflation trends that have lost a lot of their downtrend, and left inflation looking more stagnant at a pace that's above what central banks have generally targeted.