Global| Apr 07 2016

Global| Apr 07 2016Lost in Space With Deteriorating Trade Trends

Summary

While we wring our hands and gnash our teeth about what central banks are doing and the poor state of global growth, let's not forget about the internal dynamics of the EMU or about global risks. It's a very good time NOT to take our [...]

While we wring our hands and gnash our teeth about what central banks are doing and the poor state of global growth, let's not forget about the internal dynamics of the EMU or about global risks. It's a very good time NOT to take our eye of the ball of the forces that could yet rip the EMU apart (yes, I know Europeans deny it is possible- I am an unknowing American outsider.or are they in denial?).

While we wring our hands and gnash our teeth about what central banks are doing and the poor state of global growth, let's not forget about the internal dynamics of the EMU or about global risks. It's a very good time NOT to take our eye of the ball of the forces that could yet rip the EMU apart (yes, I know Europeans deny it is possible- I am an unknowing American outsider.or are they in denial?).

The competiveness key vs. trade deterioration

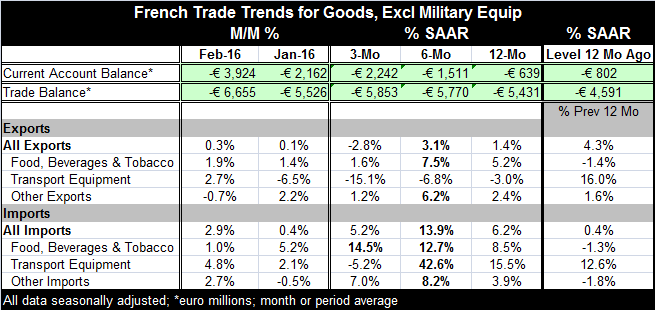

Widening differences in competitiveness among the central core countries of the EMU is one such thing that could tear at the fabric of EMU unity. We see in the table (below) that the French deficits (trade and current account) have widened markedly over the past year. In the chart, we see that both Germany and France are now seeing trade-balance deterioration. This is remarkable since the euro has been so weak on global markets (even though it has gained some purchase recently).

Export similarity/import divergence

Both German and French exports are weak with German exports up by 1.2% over 12 months and French exports up by 1.4%. But there the similarity ends. French imports are up by 6.2% while German imports are up by 3.3% (both year/year). Both growth rates show variation but also show signs of maintaining that growth gap. Such a growth gap will continue to widen the French deficit relative to that of Germany and to reduce further French growth.

EMU trade trends

EMU-wide data through January show contrary trends as in EMU exports are as weak as they are for Germany and France rising only by 1.2% over 12 months (as of January) while imports are very weak, up by only 1.1%. Manufactures imports into the EMU are up at a 3.3% pace while non-manufactures imports are falling at a 4.1% pace (commodities, oil).

But competiveness seems to be in balance

France has been overshooting its Maastricht debt parameters on the promise that it would get back into line later. Germany is running fiscal surpluses, a situation that further depresses aggregate demand in Germany. On the face of it, Germany and France do not seem to have a competitiveness gap as export growth seems about the same each place. Also France continues to hold its HICP in line with Germany's as it has since the formation of the EMU. And both show PPIs that are falling at 4% annual rate year-over-year. In some ways, France has stayed in lock-step with Germany; in other ways, it has not and is paying the price.

One leans on policy and one does not

Competitiveness does not seem to be the difference in trade performance between France and Germany, but differences in aggregate demand do seem to be at issue. France has been more eager to maintain demand with policy moves while Germany has not - or has not needed do so artificially. Germany has placed a greater priority in consolidating and advancing its already prodigious position of fiscal probity.

German-France comparisons

Compared to France, Germany has a 4.3% unemployment rate, its lowest since German reunification while France has a rate at 10.2%, a rate that has been higher only 32% of the time. The German economy is hitting on all cylinders while France is sputtering and striving to improve. France has dealt with a terrorist attack while Germany has been dealing with pesky issues of internal dissonance perpetrated by a growing (now somewhat more controlled) migrant population. Even so over the past 12 months, the German unemployment rate has dropped by 0.5 percentage points while the French rate has managed a decline of just 0.1 percentage points. Germany remains in the cat-bird seat.

Not a trade competitiveness problem but one of different type?

While France has been able to keep pace with Germany on the price front and in terms of `export competitiveness', its overall economic competitiveness has lagged as we can see by comparison of the two rates of unemployment. As a result, there is more flexibility for policy in Germany than in France and a greater overall level of consumer comfort. France is skating close to the edge on its fiscal responsibilities while Germany has a fiscal position that is among the strongest in the world. Yet, Germany is not engaged in any fiscal stimulus to help boost demand for the rest of Europe. Germany continues to violate its responsibility to reduce its external account surpluses. Since so much of that surplus is on trade within Europe, it is pushing greater deficits upon fellow EMU members, deficits that eat into their growth.

The nature of Germany's widening lead

We need to keep of these internal dynamics of the EMU in mind because it was losing track of the inflation differentials (across member countries) since the EMU was formed that substantially created the problems that ultimately developed. Germany right now has a huge lead in terms of its (1) price competiveness, (2) state of unemployment, and (3) fiscal position. Since the German economy is geared to run in this sort of sluggish growth environment (sort of like a race horse that runs well in the mud), it continues to prosper while fellow EMU members struggle, some of them still encumbered by austerity programs.

I am das rock, I am Das Island

In this environment, Germany, like Secretariat, the famed U.S. race horse, at the Belmont Stakes is opening a ridiculous lead on them. What that means is that the German economy is going to be ensconced in a currency union where it will have next to nothing in common with its fellow members. Germany will continue to be at loggerheads with the policy options that the rest of the community wants to pursue. And this is going to raise tensions across the euro area.

Not everyone plays fair

These tensions will be made worse by the conduct of German policy which is being run in such a way as to keep the rest of Europe from closing any of these gaps with Germany. Because of the `rules of the game' within the EMU, Germany has a position that gives it great power and leverage. But this is only partly due to fair play. Germany continues to refuse to adjust its external accounts from surplus to balance a key source of growing German economic and financial power.

European complications

How all of this plays out is still hard to tell. For the moment, Europe is convulsed by its migrant problem which was stoked by a generous offer by German Chancellor Angela Merkel who invited migrants to come. The rest of Germany reacted in shock and the rest of Europe acted to cut off this flow of migrants trapping them mid-stream in Greece and eventually cutting a deal to send them back to Turkey like a losing roll of the dice in a game of Migrant-opoly: "do not pass `GO' do not collect 200 deutschmarks...err euros." Once the migrant situation is better stabilized we can expect attention to turn back to economic problems. The ECB is doing all it can with the Germans overseeing every move and quick to disagree with stimulus options. The EU has no fiscal levers to pull; all of those are at the country level. So far the Maastricht (Mass-Trick?) rules have kept the fiscal side in check. But there is stirring across Europe to break out of this constraint and to do something to stimulate some real growth. It is too soon to tell if these nationalistic forces will well up to overtake what has been a solid mantle of European probity - enforced by German and other largely Northern European overseers. Europe remains in a world of hurt and the slow-changing trade position tells us that it is not getting better very fast. And the hurt is not being borne equally.

The global scene

On that score, we can turn to the WTO that today cut its forecast for the expansion of world trade. Expected growth was cut to 2.8% from 3.9% for 2016. That brings the estimate in line with the estimates for growth in each of the previous two years. Due to weak oil prices, the World Bank cut its outlook for growth in Russia to -1.9% in 2016. Oil producers are under a lot of pressure; despite their desires, they do not seem to be in position to regain pricing control anytime soon even with an upcoming meeting. If wishes were oil rigs, then pumping might slow. But they are not.

Global risks

The global economy continues to careen down this path of disequilibrium as though everything will be okay. But policy is not being driven by `The Transporter.' There is disequilibrium everywhere. And that is causing policy to cut corner and countries to cheat on the rules. The extraordinary growth in the developing world over past years has been slowed sharply cutting aspirations there and leading to unrest. Meanwhile, the shift of activity out of the developing economies to the developing world has left a gap that has resulted in growing wealth dispersion. That in turn has led to the rise of some strange political candidacies in the U.S. and elsewhere. If you think all these events are unrelated, you are only fooling yourself. The world is getting increasing interrelated, complicated, and out of kilter. Problems in one place are spreading to another and there have been no solutions. Some things that appear to be solutions in one place cause problems in another. The dangers are rising whether the Vix acknowledges it or not- so be very wary. The stock market does not discount everything.

Lost in space

It is as though we are lost in space, a space we did not expect to occupy since free trade was supposed to be a solution and lift all boats. But we never have had FREE TRADE, just the slogan. And slogans do not produce results or North Korea would be a paradise instead of being perched at the gates of hell. If we had a robot, it might say Danger, Danger, Will Robinson. But that sort of thing only happens in TV-SciFi shows, not in real life. In real life, the danger creeps up either unseen or seen and denied. If you look closely, you actually can see it creeping up. The question is this: When will we stop denying it? What will we do about it?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief