Global| Apr 11 2016

Global| Apr 11 2016Let Sleeping Dogs LEI or Wake Them and Let Them Bark?

Summary

The OECD headline index has been below 100 for six straight months and it had cultivated comparison with the Sherlock Holmes episode in which the dog `did not bark.' The LEIs are watchdogs of a sort and they are supposed to signal a [...]

The OECD headline index has been below 100 for six straight months and it had cultivated comparison with the Sherlock Holmes episode in which the dog `did not bark.' The LEIs are watchdogs of a sort and they are supposed to signal a slowing in the offing. When the OECD fails to activate its own alarm, we should begin to suspect (as did Holmes) that excessive familiarity may be the issue. OECD members have no interest in warning that their own situations may be worsening.

The OECD headline index has been below 100 for six straight months and it had cultivated comparison with the Sherlock Holmes episode in which the dog `did not bark.' The LEIs are watchdogs of a sort and they are supposed to signal a slowing in the offing. When the OECD fails to activate its own alarm, we should begin to suspect (as did Holmes) that excessive familiarity may be the issue. OECD members have no interest in warning that their own situations may be worsening.

Whatever the cause of the OECD lead-footedness this month, the OECD is off the dime and is saying that the LEI signals slowing in the region. Finally, the dog barks or at least growls.

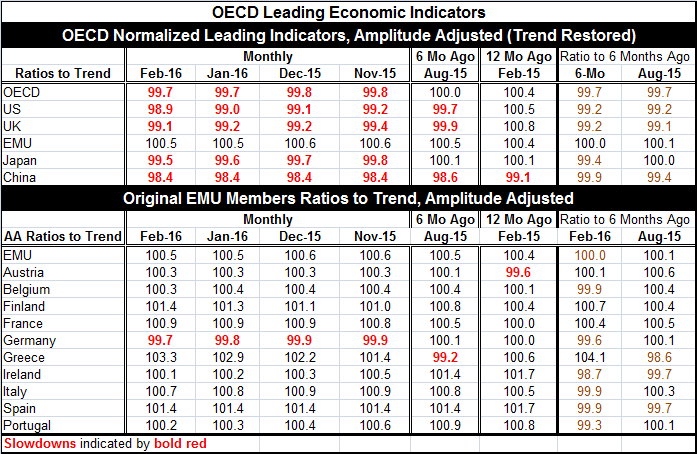

The ratio of the current OECD-area LEI to six months ago is below unity at 0.997 and the ratio of six months ago to six months before that is 0.997 as well. Counting the February level, there are now six months in a row below 100. Counting backward from February, six months ago the LEI reading was the last one not below at 100.0, in August 2015. Still, the OECD LEI is now lower over three months, six months, 12 months, and for 12 months vs. the previous 12 months. This snail's pace of a slowdown has been in place for quite some time. Despite its slow-motion speed, OECD members seem to be getting more worried about it, slow-motion or not.

The U.S. and the U.K. each have the same slowing characteristic with the February U.S. LEI gauge lower at 98.9 and the U.K. gauge lower (a bit higher level, at 99.1). For each, their six months ago LEI is higher than the current reading the six-month index before that (12 months ago) is higher than the six-month ago index signaling ongoing loss of momentum. The EMU is seen as a `zone of relative stability' with LEI readings that continue above 100 and are steady over six months and stepping higher on balance comparing six months ago to the six months before that (12 months ago).

China, like the U.S. and the U.K., also has a string of slippages and a legacy of slowdown, with its February reading at 98.4, a bit weaker than the U.S. reading. Japan with a legacy of recent readings below 100 still shows a bump up six months ago compared to the six months before that, making its slowdown a little less extended than that for the U.S., the U.K. and China.

Interestingly, the only country among the original EMU members that has persistent underperformance of its LEI in place is Germany. It also is net lower over the last six months. Greece shows the biggest ongoing pick up over six months with Finland second, France third and Austria fourth. Recall that LEIs are about `momentum' as growth assessments are compared to past standards. On those grounds, Germany is indeed doing worse than it does historically and Greece (that has done so badly historically) is doing- not well- but better than it has done recently under all its austerity programs. Greece is not about to become the engine of growth for Europe; be sure to understand this `signal' for what it is (and isn't).

Of course, countries also have their own LEIs and the Conference Board offers up a set of relatively comprehensive metrics. Its view of the U.S. economy has been showing some weakness in its LEI. The U.S. LEI expansion is not raising any real warning flags on growth per se, but the LEI is growing at a substandard pace.

On balance, the IMF has been instrumental in trying to sound the call to ward off complacency and to make sure that this period of weakness does not culminate in something worse. Recent forecasts continue to be cut. Most recently the World Bank (today) trimmed its growth outlook for East Asia. Also today the German economic ministry announced that it looked for the expansion to continue at a somewhat slower pace, noting that the environment is subdued. In the U.K., the Chamber of Commerce noted a loss in momentum for U.K. growth. In the last several weeks, U.S. FOMC members have cut their outlooks as well, reducing the expected path for the fed funds rate ahead. There are a number of straws in the wind about economic slowing. The OECD gauges do not stand alone, and they no longer stand mute.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief