Global| Apr 05 2016

Global| Apr 05 2016German Orders Drop Unexpectedly Exposing It As a Free Rider

Summary

On a day IMF Managing Director Christine Lagarde had chosen to rebuke the industrialized nations on their need to do more to stimulate global growth, German industrial orders have fallen largely because of weakness in orders overseas. [...]

On a day IMF Managing Director Christine Lagarde had chosen to rebuke the industrialized nations on their need to do more to stimulate global growth, German industrial orders have fallen largely because of weakness in orders overseas. If any country epitomizes the need to `do more' in this global environment, it is Germany whose `finely tuned economy' is geared to sop up the domestic demand in other markets and grind out its growth on the bones of that framework. Germany ran a financial surplus in 2015 when the rest of the EMU was struggling with debt to meets largely German-enforced debt rules under the Maastricht criterion of the EU/EMU. There would be no corner-cutting to acknowledge tough economic times under German policy tutelage. Germany has the financial flexibility to do more itself, but it has not. It has consistently blocked or delayed attempts by the ECB to engage in more stimulus and put fellow EMU member countries' feet to the fire over meeting their Maastricht pledges regardless of events. German negotiators went so far as to suggest Greece should get no slack under its debt agreement for all the funds it has expending by laboring under the stresses of a flood of migrants that have landed on its shores had to be cared for. Really! The Germans have been the disrupters of growth in the EMU under the guise of being the good guys. Well, these days it's hard to tell who is wearing the white hats. Unrelenting fiscal and monetary rules may not work best for all countries at all times.

On a day IMF Managing Director Christine Lagarde had chosen to rebuke the industrialized nations on their need to do more to stimulate global growth, German industrial orders have fallen largely because of weakness in orders overseas. If any country epitomizes the need to `do more' in this global environment, it is Germany whose `finely tuned economy' is geared to sop up the domestic demand in other markets and grind out its growth on the bones of that framework. Germany ran a financial surplus in 2015 when the rest of the EMU was struggling with debt to meets largely German-enforced debt rules under the Maastricht criterion of the EU/EMU. There would be no corner-cutting to acknowledge tough economic times under German policy tutelage. Germany has the financial flexibility to do more itself, but it has not. It has consistently blocked or delayed attempts by the ECB to engage in more stimulus and put fellow EMU member countries' feet to the fire over meeting their Maastricht pledges regardless of events. German negotiators went so far as to suggest Greece should get no slack under its debt agreement for all the funds it has expending by laboring under the stresses of a flood of migrants that have landed on its shores had to be cared for. Really! The Germans have been the disrupters of growth in the EMU under the guise of being the good guys. Well, these days it's hard to tell who is wearing the white hats. Unrelenting fiscal and monetary rules may not work best for all countries at all times.

The data

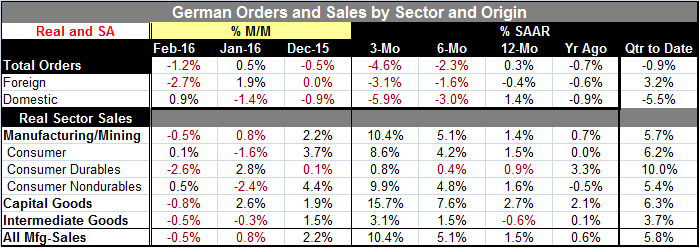

German orders fell by 1.2% in February after a tepid 0.5% increase in January. Foreign sourced orders fell by 2.7% to drive total orders swamping a 0.9% rise in domestic orders. As of February, total orders, foreign orders and domestic orders each are showing outright declines over three-months and six-months. The declines for each series show steady decelerations in play across each category for growth rates calculated over three-months compared to six-months, for six-months compared to 12-months. In the quarter-to-date period, overall orders are falling and domestic orders are falling, but foreign orders still are on the rise.

Real sector sales

The picture for real sector sales shows some recent sputtering but does not show as clearly the weakness we see in the German order trends. That is not surprising since the weakness is mostly emanating from overseas orders. Real sector sales have become spotty over the last few months as mining and manufacturing sales fell in February after a decelerating gain in January. In February, sales fall in two of three main manufacturing sectors: capital goods and intermediate goods; consumer goods sales are edging up by 0.1%, the thinnest of possible margins. Still, over three-months real sector sales are up at a 10.4% pace with no sector-level declines in play. In fact, overall sector sales are steadily accelerating in all major categories as of February.

The IMF is not happy

The IMF today sounded as if it were ready to cut its outlook again. It is concerned that too much growth has been on the back of developing nations and cites the shift in China to a more demand-dependent economy as creating some irregular heart rhythms for growth during the shift-over. The IMF calls the economic expansion frail. It looks for the most industrialized nations to do more.

Germany has taken this opportunity to puts its fiscal house into surplus, a growth contracting mode. Germany already benefits from being in a currency union. Germany has huge trade and current account surpluses, especially as a ratio to GDP. Yet, since it is exporting out of a zone using a very weak common-currency, Germany's export success is enhanced. Germany is continuing to run extremely low inflation rates in the EMU to cement and extend its competitiveness advantage. Its February -0.2% HICP (y/y) ranks as the time third lowest pace among original EMU members. Since forming the EMU, Germany has acquired a double-digit price advantage in percentage terms vs. six of the original 11 members (includes Greece). Germany continues to press its advantage. It is not trying to integrate. It is making sure that it keeps and extends its advantages even as Europe is in a state of distress.

The German way or the highway...(autobahn or woe-be-gone?)

Moreover, Germany's attempt to export German values is not working. The Scandinavian countries have tried extending their system to foreigners by allowing them to settle with full rights and they find that the social welfare system is so complete that foreigners are happy just to hunker down and accept endless Government payments. The lesson that is not learned by the Germans is that economic policy is part of a nation's social compact. You cannot simply impose it or apply to another people. The real problem is that austerity does not work unless it is 24-7:365 proposition. And many countries having been under the yoke of austerity cannot wait to get off of it. Some are trying to get out of the constraints even now while they are still not eligible to leave austerity programs. But since everyone in the EMU is bound together under the same exchange rate, there is really no other way.

The policy trap

The rest of Europe did not see this coming into the EMU. The ECB had no mechanism to equalize national rates of inflation so Germany by running below target inflation (with its large GDP weight) meant that excesses could build in smaller nations for quite some time. On balance, the EMU has not been very honest with its members about the cost of membership. It may now be more apparent to those who would join. But it should be clear that Germany will run its policies in the way that is best for Germany and it will not swerve to help other members on policy. Compromise means doing it the German way. There are no alternatives. The Germans helped to carefully write the rules and they zealously enforce them. Germany may throw in some money in the pot when problems emerge. But policy is not to be touched. This is how Germany finds itself as an outsider despite being a clear insider. Germany is apart from the EMU on too many measures. It has the lowest budget deficit (has a surplus), lowest rate unemployment, lowest inflation rate and largest trade deficit which it refuses to adjust. Yes, it works for Germany, but it doesn't export well or fit well into a common European scheme. Yet, it all leaves Germany in complete control of Europe.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief