Global| Nov 08 2017

Global| Nov 08 2017French Deficits Widen But Do No Harm

Summary

In September, French exports barely nudged ahead as imports gained 1.2% expanding the trade deficit to 6.4 billion euros from 5.9 billion euros in August. On a broader timeline, imports have been outpacing exports since early-2016 on [...]

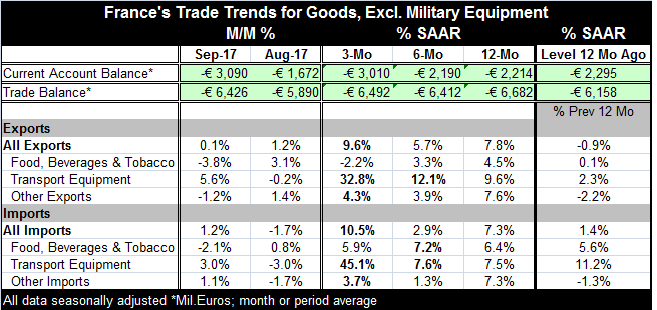

In September, French exports barely nudged ahead as imports gained 1.2% expanding the trade deficit to 6.4 billion euros from 5.9 billion euros in August. On a broader timeline, imports have been outpacing exports since early-2016 on a regular basis. On that timeline, the French deficits have been steadily eroding. In this episode of deficit erosion, both French exports and imports are on accelerating trends. One year ago, exports were falling at a 0.9% annual rate. Currently, exports are expanding by 7.8% over the last year. One year ago, imports were rising at a lackluster 1.4% pace. Currently, they are gaining 7.3% over 12 months.

In September, French exports barely nudged ahead as imports gained 1.2% expanding the trade deficit to 6.4 billion euros from 5.9 billion euros in August. On a broader timeline, imports have been outpacing exports since early-2016 on a regular basis. On that timeline, the French deficits have been steadily eroding. In this episode of deficit erosion, both French exports and imports are on accelerating trends. One year ago, exports were falling at a 0.9% annual rate. Currently, exports are expanding by 7.8% over the last year. One year ago, imports were rising at a lackluster 1.4% pace. Currently, they are gaining 7.3% over 12 months.

As exports and imports have steadied their pace in the last two months, export growth has caught up to import growth. Export growth is just a shade higher than import growth in each of the last two months in terms of 12-month rates of growth. But over the last 18 months, that has only happened four times. The current margin of exports over imports is negligible. However, since exports are only about 86% of imports, they have to grow about 14% faster than imports to keep the trade deficit steady. So if imports are growing at about 8% year-on-year, exports would have to grow by between 9% and 9.5% to keep the deficit steady in nominal terms. And that is not happening; the French deficit is still widening year-on-year.

However, there is no clear export or import shifting of gears. Both exports and imports are growing faster over three months than over 12 months, but both also log an intermediate six-month pace that is weaker than the year-on-year pace before speeding up over three months. So there is no clear acceleration in either exports or imports from 12 months to three months.

Within exports, foods exports are accelerating and transportation equipment exports are accelerating and surging over three months. But the 'other' category, which is the largest, shows an irregular slowing.

For imports, food trends are unclear, but they are probably best characterized as trendless and steady with some volatility. Transportation equipment trends mirror the export side with strength building and growth on an explosive three-month gain. However, the large 'other' category shows no trend, but as with exports it shows weaker growth over both three months and six months than over 12 months.

The acceleration in French trade flows is an artifact of souped-up trade in transportation equipment. And those flows can be volatile. French trade is probably better categorized by the slowing trends in both exports and imports in 'other' trade group even though that does not dominate the overall growth picture for the month.

The French economy is still doing well. Its PMI survey that extends into October shows a better performing manufacturing and services sector. Clearly, manufacturing is doing well and the buoyant services sector signals that imports should remain lively boosted by domestic demand. Recent German export orders showed strong demand for German exports from within the EMU suggesting that growth in the EMU-area remains solid too creating a good environment for mutually beneficial trade. The EMU-wide PMIs have continued to show solid and widespread expansion. French trade flows are now growing at a very similar pace for exports and imports. And the shift in the deficit has exhibited only slow erosion. Trade does not appear to be either a large positive or negative for the French economy in terms of its ongoing cyclical impact.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief