Global| Apr 13 2016

Global| Apr 13 2016Euro Area IP Falls After January Spurt... and Remains on Growth Path

Summary

Awfully good results for a flawed pattern of growth February industrial output has fallen and is lower in two of the last three months with measurable positive gains in only four of the last 12 months and with manufacturing output [...]

Awfully good results for a flawed pattern of growth

Awfully good results for a flawed pattern of growth

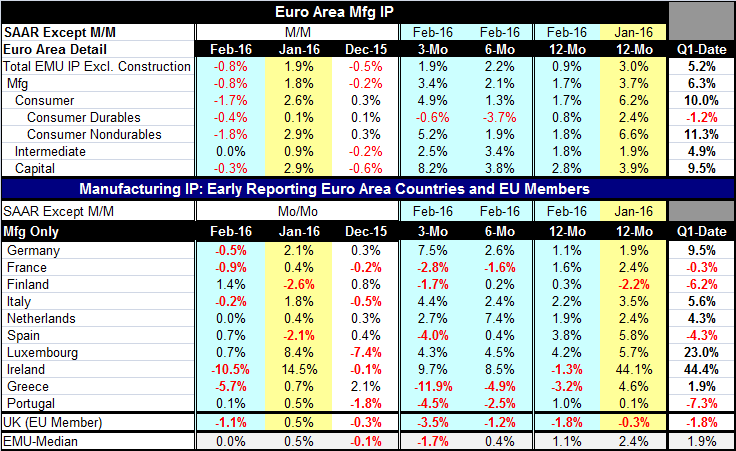

February industrial output has fallen and is lower in two of the last three months with measurable positive gains in only four of the last 12 months and with manufacturing output lower in five of the last seven months. These seem to be substantial strings of weakness. And spottiness is one of the problems dogging output in the EMU. Output gains, however, scattered, have been substantial when they have occurred.

Sector trends are astonishingly good

Output overall as well as for manufacturing in the EMU is currently rising on all three major horizons, over three-month, six- month and 12-month. By sector, output is rising on all horizons as well. The only exception is the subsector of durable goods under consumption which has a net decline in output over both three-month and six-month. But strength in nondurables pulls that up so that output for all consumer goods is still rising on all horizons. In fact, the output of capital goods is accelerating, rising for a 2.8% rate of growth over 12-month to a 3.8% pace over six-month to 8.2% over three-month. Intermediate goods output also is on an accelerating path. Manufacturing looks pretty healthy in its sector behavior.

Manufacturing looks solid

Manufacturing IP is accelerating steadily from 12-month to six-month to three-month despite weakness in consumer durable goods. Even with episodes of monthly weakness in manufacturing, the EMU continues to show consistent gains on reasonably solid growth rates. Still, the spottiness of the pattern remains an impediment to trusting the trend too much.

Quarter-to-date growth is solid

In the quarter-to-date, output and manufacturing are up at growth rates in excess of 5% annualized. Part of this `strength' is the weak base that these calculations spring from. Manufacturing output fell in each of the three months of the fourth quarter while overall output made no discernable gain in any month of the quarter with clear drops in two out of three. That base effect dresses up the increases reported in Q1.

Country by Country

Looking at the results out of the reporting first EMU members (10 here), we see output declines in half of them in February and declines in four out of 10 in the quarter-to-date. There also are output declines in half of them over the recent three months. But the story here obviously parallels the story of strength for output as a whole. For the most part, the output gains are either larger than the losses or the gains are coming from countries with larger weights while losses are coming from countries with smaller weights. France is a large country with persistent output drops. But Germany has persistent increases apart from a decline in February. Italy and Spain mostly show output increases.

Good results amid global weakness

The global industrial sector is well integrated through trade so it is hard for even the most competitive country to swim against the current if globally the sector remains under pressure. And we continue to see a host of weakness in manufacturing PMI data globally. However, today China reported a sharp increase in its exports from its lunar-year-affected low. Global trade data which speak directly to the goods and therefor the manufacturing sector continues to be distressed. The WTO recently cut its outlook for trade expansion. Against such a background European manufacturing is not doing so poorly. But the context also warns us not to expect too much of it. The global services sector is only holding in the lower 14th percentile of its historic range (back to October 2008). That is not much to fall back on. Meanwhile, (also since October 2008) EMU manufacturing has a 57th percentile standing, the U.S. manufacturing sector, a 32nd percentile standing, Japan, a 17th percentile standing, and emerging markets register a 47th percentile standing - with China given a 54th percentile and the BRIC countries averaging a 31st percentile standing. That is a lot of weakness/moderation and of course there is no strength there anywhere.

As banks take their lumps...

These metrics remind us of global weakness. Meanwhile Italy has adopted a new fund to backstop its banks while banks in the U.S. are starting to get hit by energy-sector losses. Global bank lending has been weak to moderate except in China.

Outlooks are muddled

The outlook for growth remains weak. Growth outlooks have been downgraded by the IMF, the WTO, the German Economics Ministry, the U.K. Chamber of Commerce and by the FOMC members in the U.S. There are risks to growth from the potential for Brexit and possibly from an upcoming OPEC meeting. That's a pretty broad and diverse grouping of factors. For the most part, however, growth downgrades have been small. While downgrades for growth continue the various forecasting agencies seem reluctant to cut their projections too much. The downgrades are more like `window dressing' or `warnings.'

The policy of policy

Some in the U.S. continue to think that the weak path of GDP is a statistical anomaly and want the Fed to press ahead with four rate hikes even in the aftermath of the Fed Chair's recent guidance to a milder path (the Richmond Fed's Jeffrey Lacker among others). Clearly this is an environment that cultivates different views. It is also one where forecast errors have been large and persistent. What seems foolish is anyone's notion that they can be sure of what happens next. Policy clearly is hampered as so much ammunition been expended with such little effect. If the next step for growth is backward there is not as much support that policy can offer despite some confident statements made by central bankers about the role that QE could still play.

Policy should step lightly

Policy in this environment should continue to step softly and try to nurture growth until prospects seem more certain. `If the roots are strong, there will be growth in the spring.' That was the view of Chance Gardener in the movie, `Being There.' That view may still hold here, but it would be good to get some confirmation first. Risks still abound. There is a pending greater-OPEC meeting with uncertain prospects amid more uncertain prospects for the path of oil prices. There is uncertainty about China. And many a central bank has made a step forward in this cycle only to have to step back or go to hold. There should be some learning from that and caution as a result. Bankers would do well to remember that despite making forecasts, they do not know what they do not know...

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief